{kind=link}

Handing your friend a $10 bill (or writing them a check) is a reasonably efficient way to settle a single debt.

When your transactions number in the hundreds, however—and your debtors and credits are spread across the United States—paper checks become a much less efficient way to receive and send money.

The Automated Clearing House (ACH) network solves this problem by facilitating electronic transfers between financial institutions.

Table of Contents

What is the Automated Clearing House?

The Automated Clearing House is an electronic network for processing electronic payments between banks. The ACH network is maintained by an organization called NACHA, or the National Automated Clearing House Association, a 501(c)(6)not-for-profitassociation connected to some 11,000 different financial institutions.

The need for NACHA was identified in 1968, when a group of bankers in California noted the increasing volume of paper checks they were handling and processing. These bankers organized the Special Committee on Paperless Entries, or SCOPE, and, in 1972, formed the first ACH organization in California to handle electronic payment processing. NACHA followed in 1974.

NACHA manages everything pertaining to the maintenance, development, and administration of the ACH network, which has become the primary mechanism for handling financial transactions electronically in the United States. Every year, it facilitates the payment of billions of dollars pertaining to business, government, and consumer needs.

What are ACH payments?

空调采暖支付是电子资金转移过程ed through the Automated Clearing House network. They enable businesses and consumers to send and receive payments in a fast, secure, and cost-effective manner. ACH payments are commonly used for direct deposit payrolls, bill payments, and transferring funds between bank accounts.

How much does it cost to use and accept ACH payments?

上述支付费用可以在许多计算ways—either as a flat fee per transaction, as a percentage of a transaction, or as a monthly cost. If you choose to accept ACH payments directly, your bank will determine the fees owed. Transfers such as bill payments, payroll direct deposits, and direct payments are often free of charge.

Many business owners also choose to work with third-partypayment processors(such as PayPal, Stripe, Square, or others) to process business-to-business and business-to-consumer transactions. In this case, the third-party payment processor determines the cost of the transaction, with typical ACH transfer fees ranging from 0.8% to 1.5% of total transaction cost.

How are typical ACH payment processing times?

It can take between one to 23 business days to process ACH payments. The exact time depends on the transaction type and when it is submitted.

ACH transactions are batch-processed multiple times a day, ensuring efficient payment processing and settlement between financial institutions, ultimately resulting in faster access to funds for businesses and individuals.

Direct deposit vs. direct payment

ACH transactions can be broadly classified into two main categories: direct deposits and direct payments.

- ACH direct deposits:These transactions are where funds are transferred from the originator’s account to a receiver’s account. They are used for payroll, government benefits, interest payments, and tax refunds.

- ACH direct payments:These are transactions that are transferred from a payer’s account to a payee’s account to make payments or settle bills.

Direct payments are often used in business-to-business (B2B) transactions, such as making payments to suppliers or transferring funds between business accounts.

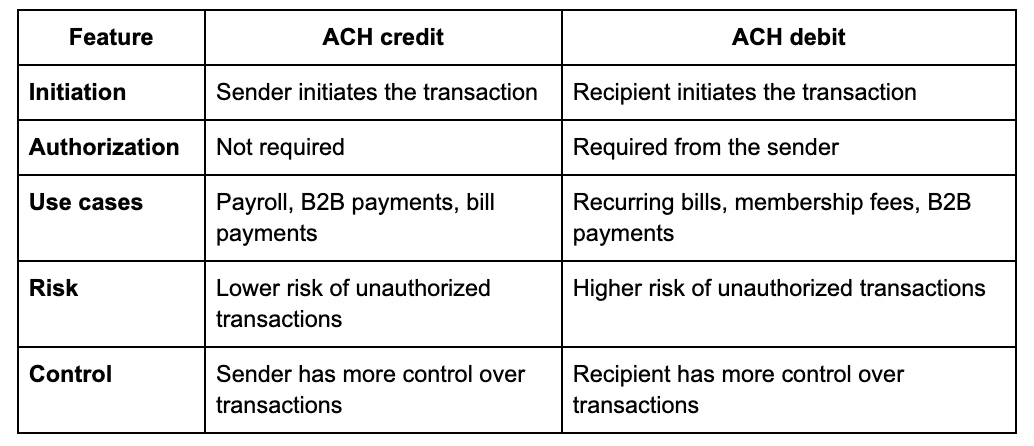

ACH credit vs. ACH debit

There are two main types of ACH transfers, ACH credit and ACH debit.

ACH credit transactions involve the transfer of funds from the sender’s bank account to the recipient’s bank account.

ACH credit is used for:

- Direct deposit of payroll, Social Security benefits, and tax refunds

- Business-to-business payments

- Bill payments initiated by the payer

ACH debit transactions involve the transfer of funds from the recipient’s bank account to the sender’s bank account.

ACH debit is used for:

- 反复出现的账单支付,如公用事业,mortgages, and loans

- Membership fees and subscription payments

- Business-to-business transactions initiated by the payee

How does the ACH work?

The Automated Clearing House network serves as an intermediary between financial institutions—allowing banks, businesses, and institutions to send money electronically. The ACH network organizes and processes a type ofelectronic funds transferknown as anACH transfer.

Here’s an example of how a direct deposit payment process using ACH works:

- The originating party (in this case, the employer) initiates a payment, like its employee’s biweekly paychecks. Employees just need to give the employer their checking account information (account number and routing number) to receive ACH transactions.

- The originator’s bank (also known as ODFI, short for originating depository financial institution) batches the transaction along with other ACH bank transfers. These batched transactions are sent out at regular intervals during the business day.

- An ACH operator (either the Federal Reserve or the Electronic Payments Network) receives the batched transactions, sorts them, and submits the transactions to the receiving depository financial institution (RDFI).

- The receiving bank account processes the transaction and credits the receiving account (that of the employee).

All ACH transfers are categorized as eithercredit or debit transactions,with the classification being determined by the action of the originating party.

直接存款,例如,信用卡诈骗罪red a credit transaction because the originating party is moving money from their account to the recipient’s bank account, resulting in a debit from the originating account and a credit to the receiving account.

Benefits of ACH

Cost

One advantage of sending and accepting ACH payments is cost savings. Using ACH transfers to receive and send money allows companies to avoid paying credit card transaction fees, which can total up to 2.5% of the total transaction value.

On a $10,000 sale, that’s $250—and because sales amounts cover operating costs andcost of goods sold, this fee can significantly eat into your profit margin. If your net profit on a $10,000 sale is $3,000, for example, a 2.5% credit card fee reduces your profit by 8.3%.

Security

ACH payments offer security advantages over both paper checks and cash. Checks can go missing in the mail, and large amounts of cash require advanced security measures to discourage theft—think security guards and armored trucks.

Electronic payments are less vulnerable, and ACH payments provide an additional advantage over instant transfers: their one-to-three-day processing time provides a buffer during which businesses can stop payment if fraud is suspected or an error is identified.

Convenience

Electronic processing of ACH payments makes it easy to set uprecurring paymentsto vendors or employees, cutting down on your administrative burden and reducing operating costs. Customers and employees also appreciate the ease of ACH payments.

Cons of ACH

Processing times

Because ACH transfers are processed in batches, direct ACH payments are not processed instantly. It can take one to three business days for a transfer to appear in a recipient’s bank account once it is initiated.

Some banks also allow for same-day ACH transfers, which may be available for an additional fee. Note, however, that processing cutoff times may result in same-day transfers processing during the next business day.

Some third-party processors allow for instant ACH transfers by crediting money to a receiving account immediately within the processing app, then reconciling the accounts through the ACH transaction process at a later date. These processors may also have “instant” transfer options available.

No international payments

ACH payments can only be deposited into United States bank and credit union accounts. International money transfers require businesses to use wire transfers or other methods such as mailing a paper check or initiating a transfer via a third-party payment processor.

Transaction limits

Some banks impose daily, weekly, monthly, or per-transaction limits on the amount of money that can be sent through the ACH system. For example, savings accounts are governed byFederal Reserve Regulation D, which limits certain withdrawals or transfers to six per month. If you go over the limit, you could get hit with a penalty.

Check with your bank to make sure that its policies support the kind of transfers you need to support your business operations.

Use ACH to settle payments faster for your small business

The business world moves fast—and writing a paper check or paying with a debit card is a frustrating process. A world where you can pay your subway fare with a tap of your credit card and purchase your groceries through fingerprint recognition is one where efficiency is key—for both your business and your customers.

ACH transfers offer increased security and convenience for both creditors and recipients at a relatively low cost. Your bank (or a third-party processor) can make sending and receiving payments an efficient and low-cost aspect of your business operations.

Ready to create your business? Start your free trial of Shopify—no credit card required.

ACH payments FAQ

What is an ACH in banking?

What is the difference between direct deposit and ACH?

What are examples of ACH payments?

- Direct deposit: ACH payments are commonly used for direct deposits of payroll or other payments from employers to employees.

- Bill payments: Many utility companies, credit card companies, and other service providers allow customers to pay their bills via ACH payments.

- Online shopping: Many online retailers, such as Amazon, accept ACH payments as a payment method.

- Peer-to-peer payments: ACH payments are often used to transfer funds between individuals, such as friends or family members.

- Charitable donations: ACH payments are commonly used to donate money to charities and other nonprofit organizations.